Abstract

Formula 1 entered 2017 as a sport in structural decline, having shed 40% of its global television audience over the preceding eight years. By 2025, it had generated $3.87 billion in annual revenue, which is a 115% increase, and grown its global fanbase to 827 million people, with 42% now identifying as women (compared with 8% in 2017). This study argues that the transformation was not driven by changes to the sporting product, the technology, or the rules. It was driven by a deliberate, sustained content strategy built around one premise: tell stories for people who have never heard of you yet.

The study proceeds in three analytical layers. Layer 1 documents the F1 financial and demographic transformation with granular data. Layer 2 situates this transformation within the broader $525 billion global content marketing landscape, establishing the universal commercial logic behind the audience-first strategy. Layer 3 examines the emerging AI search shift, the structural change that makes content strategy more urgent, not less, in 2025 and beyond. The study concludes with a synthesis: the convergence of self-directed buyer behavior, AI-mediated discovery, and demographic transformation means that content is no longer a channel. It is the foundation on which commercial relationships are built before a single conversation takes place.

01

The Premise: A Sport That Was Slowly Dying

1.1 The State of Formula 1 Before Liberty Media

There is a version of this story in which Formula 1 fades gracefully into irrelevance. By 2016, the sport had lost 40% of its global television audience compared with 2008 (Liberty Media Corporation, 2017). The drivers wore helmets that obscured their faces. The cars were engineered for lap-time supremacy rather than on-track drama. The commercial structure was closed: broadcasting deals were locked behind pay-TV walls, digital content was restricted, and social media was actively discouraged by the sport’s governing bodies. A new generation of sports fans raised on the raw access of social media, on the parasocial intimacy of YouTube and podcasting, on stories rather than statistics, looked at Formula 1 and saw a logo, not a story.

The product itself was extraordinary. The engineering was unmatched. The circuits were beautiful. But nobody outside the existing fanbase knew why they should care. Formula 1 had made the classical error that many businesses make: it was speaking exclusively to people who already loved it, with language only they could understand.

1.2 The Acquisition Thesis

In January 2017, Liberty Media Corporation completed its $4.4 billion acquisition of Formula 1’s equity, implying an enterprise value of approximately $8 billion (Liberty Media Corporation Annual Report, 2017). The transaction was considered fairly priced — a stable business with dependable media rights income, bought at a reasonable multiple. What Liberty saw, however, was not a stable business. It was a massively undervalued storytelling asset.

The new commercial leadership, particularly Sean Bratches as Managing Director of Commercial Operations, understood something fundamental: the emotional infrastructure of a global sport was already built. The drivers had rivalries, personalities, and drama. The teams had histories. The circuits had character. None of it was being communicated to people who might fall in love with it. The intervention required was not engineering. It was storytelling.

“

F1 didn’t build a better car to grow its revenue. It built a better audience. That is the only lesson that matters.

DATA LAYER 1

The F1 Transformation Story

2.1 Revenue: The Numbers That Define a Turnaround

When Liberty Media completed its acquisition in January 2017, Formula 1 generated approximately $1.8 billion in annual revenue. By 2025, that figure had grown to $3.87 billion, which is a 115% increase in eight years (BlackBook Motorsport, 2026; Liberty Media Corporation, 2025).

Operating income for the same year came in at $632 million, up 28% year-on-year. Fan attendance across all 24 races reached 6.75 million people, a 4% increase on 2024.

Source: Liberty Media Corporation Annual Reports 2017–2025 (NASDAQ: FWONA); BlackBook Motorsport (March 2026); S&P Global Market Intelligence (August 2025).

The revenue structure itself is revealing. Three primary streams divide the income: media rights fees (31.3%), race promotion revenue (26.7%), and sponsorship fees (21.7%), with the remaining 20.3% from hospitality, freight, and licensing (Liberty Media, 2025). Crucially, 2025 marked the first year that sponsorship exceeded 20% of primary revenue since Liberty’s acquisition; a direct indicator of the sport’s increased commercial attractiveness to new categories of brands (BlackBook Motorsport, 2026). Brands do not pay more to reach the same audience. They pay more when the audience changes.

| Metric | 2017 | 2024 | 2025 | Change |

|---|---|---|---|---|

| Total Revenue | ~$1.8 billion | $3.41 billion | $3.87 billion | +115% |

| Operating Income | ~$200M est. | $492 million | $632 million | +216% est. |

| Media Rights Revenue | $606.6 million | $1.07 billion | ~$1.21 billion | +100% |

| Race Calendar (events) | 20 races | 24 races | 24 races | +20% |

| Fan Attendance (total) | ~5M est. | ~6.5M | ~6.75M | +35% est. |

Table 1: Formula 1 Key Financial Metrics, 2017–2025. Source: Liberty Media Corporation Annual Reports; S&P Global Market Intelligence; BlackBook Motorsport.

2.2 Drive to Survive: The Documentary That Built an Audience

Formula 1: Drive to Survive premiered on Netflix in March 2019. To describe it merely as a documentary is to misunderstand what it was strategically. Sean Bratches and the Liberty Media commercial team had identified a specific problem: the sport’s existing broadcast coverage assumed knowledge. Commentators explained DRS, KERS, and tyre compounds to audiences who were already fans. Nobody was making content for the person who had never watched a Grand Prix and had no reason to start.

Drive to Survive changed that. By following drivers and team principals through an entire season in hotel rooms, in garages, in moments of failure and triumph, it did not explain the sport. It made people feel the sport. The difference is the entire argument of this study.

| Season | Release | Peak Viewership | Key Context |

|---|---|---|---|

| Season 1 | March 2019 | ~288K unique viewers (Wk 1) | Launch — Mercedes & Ferrari did not participate |

| Season 2 | Feb 2020 | Growth vs S1 | Pre-pandemic momentum building |

| Season 3 | March 2021 | ~266K unique viewers (Wk 1) | Pandemic era; US audience surging |

| Season 4 | March 2022 | 1.5M viewers; 29M hours (peak week) | Hamilton/Verstappen title fight — all-time peak |

| Season 5 | Feb 2023 | 26.2M hours peak; 644K Wk 1 | Highest opening week at the time |

| Season 6 | Feb 2024 | 28.1M hours peak | 11.6M views/episode average (Feb–Jun 2024) |

| Season 7 | March 2025 | 22.9M hours (Wk 2 peak) | Won Sports Emmy, Outstanding Documentary 2025 |

| Season 8 | Feb 2026 | 18.5M hours (Wk 2, #5 globally) | Consistent global top-10 performance |

Table 2: Drive to Survive — Viewership by Season. Source: Plum Research/ShowLabs; Netflix official data; Parrot Analytics; Domo Season 8 Analysis (May 2026).

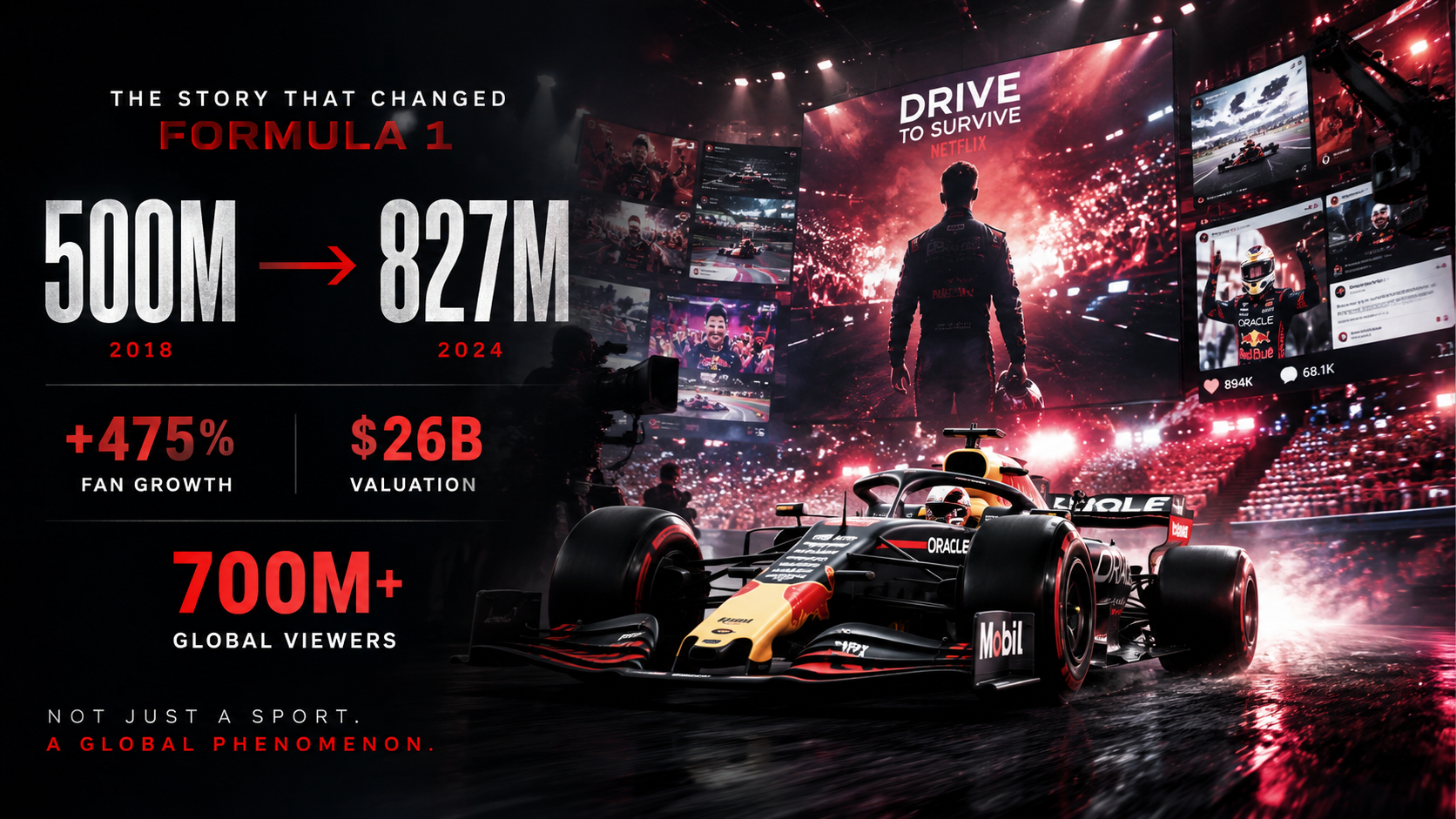

The cumulative impact is now documented at over 700 million viewers worldwide since the series launched, a figure sourced directly from Formula1.com (Formula1.com, 2025). For context: that number is larger than the entire population of Europe. A single piece of content, structured as a story rather than a broadcast, reached more people in six years than the sport’s traditional coverage had reached in decades.

700M+Cumulative Drive to Survive viewers worldwide

8Seasons produced by 2026

2025Sports Emmy won for Outstanding Documentary

Source: Formula1.com (2025); Netflix official data; Television Academy Sports Emmy Awards (2025).

2.3 The United States: A 1,500% Proof-of-Concept

No single market demonstrates the content strategy thesis more cleanly than the United States. Before Liberty Media’s acquisition, American motorsport culture was dominated by NASCAR and IndyCar. Formula 1 had a niche, loyal audience, but negligible mainstream penetration. When ESPN acquired US broadcast rights in 2018, the deal was struck for approximately $5 million per year, which is a figure so low that Liberty had initially attempted to give the rights away for free after negotiations with NBC collapsed (S&P Global Market Intelligence, 2025).

$5M

ESPN US rights deal 2018

ESPN US rights deal 2018

→

Content strategy plays out

Content strategy plays out

$90M

ESPN US rights deal 2023

ESPN US rights deal 2023

By 2023, the same broadcast rights commanded $75–90 million per year: a 1,500% increase driven entirely by audience growth that Drive to Survive had catalyzed (S&P Global, 2025). This is the commercial proof of the content thesis: Content doesn’t just build awareness. It builds leverage that compounds into hard commercial value.

547KAvg. US viewers/race 2018 (pre-Drive to Survive)

1.3MAvg. US viewers/race 2022 (record high)

+120%US viewership growth 2018 to 2022

1,500%ESPN rights value increase 2018 to 2023

Source: ESPN broadcast data; S&P Global Market Intelligence (August 2025); Nielsen Fan Insights (May 2022).

Nielsen’s own analysis of the Drive to Survive effect is perhaps the most granular data point in this entire study. In a 2022 study, Nielsen found that 34% of Drive to Survive viewers in the US became F1 fans after watching the series (Nielsen Fan Insights, 2022). A further 30% reported they understood the sport better, 29% said they felt more engaged, and 22% of all current F1 fans cite the series as a major reason they started following the sport. Nielsen also tracked that more than 360,000 people who had not watched F1 in late 2021 became new fans ahead of the 2022 Miami Grand Prix — directly following their viewing of Drive to Survive.

US F1 fans grew from approximately 44.9 million in 2019 to 49.2 million by 2022, a 10% increase in three years in a country where the sport had struggled for decades (Nielsen Fan Insights, 2022; S&P Global, 2025). Content didn’t just build awareness. It created commercial leverage that multiplied media rights value by fifteen times.

2.4 The Demographic Earthquake

Of all Formula 1’s growth metrics, the demographic transformation is analytically the most significant because it represents a structural change, not a cyclical one. These data come from F1’s own Global Fan Survey, conducted with Motorsport Network in 2025, drawing on over 100,000 responses from 186 countries (F1/Motorsport Network, 2025).

| Metric | 2017/2018 Baseline | 2025 Figure | Change |

|---|---|---|---|

| Female fans (% of total fanbase) | 8% | 42% | +34% points |

| Women as a share of NEW fans | Minority | 3 in 4 | High change (now 75%) |

| Fans under 35 | ~30% est. | 43% | +13% points |

| Average fan age | 36 years | 32 years (by 2021) | −4 years |

| Gen Z as % of highly engaged fans | — | 27% | New primary cohort |

| Gen Z daily F1 content engagement (US) | — | 70% | Always-on fandom |

| Social media followers (all platforms) | 18.7M (2018) | 107.6M | +475% |

| Global fanbase total | ~500M est. | 827 million | +12% last year alone |

Table 3: F1 Demographic Transformation, 2017–2025. Source: F1/Motorsport Network Global Fan Survey 2025 (100,000+ responses, 186 countries); Newsweek (August 2025); Comscore (April 2025); F1 CEO Stefano Domenicali public statements.

8%→42%Female fanbase in 8 years

827MGlobal fanbase 2025

+475%Social media following

27%Gen Z among highly engaged fans

Jon Stainer, Global General Manager at Nielsen Sports, attributed the shift directly to storytelling: ‘Growth of interest, especially among women, can be attributed largely to a shift in how the teams and drivers are profiled today, and the access they are affording global audiences’ (Nielsen Sports Annual Report, 2024).

Nearly half of Gen Z respondents in the 2025 survey identified as women. F1 was a sport that spoke to people who already loved cars. Now it speaks to people who love stories. The product did not change. The storytelling did.

“

The product didn’t change. The storytelling did. That single shift moved the female fanbase from 8% to 42% in eight years.

2.5 Brand Valuation as the Final Verdict

Brand valuation is the market’s aggregated verdict on the future value of a business. In January 2017, Liberty Media paid $4.4 billion for F1’s equity, implying an enterprise value of approximately $8 billion — widely considered fair value at the time (Liberty Media Corporation, 2017; Forbes, 2017). As of 2025, F1 equity trades at approximately $90 per share, placing the enterprise value at over $26 billion, a 225% increase, or a 16% annualised return, in eight years (Liberty Media Q4 2025 Earnings; Forbes).

| Asset / Metric | Pre-Liberty (2016–17) | 2024–2025 | Growth |

|---|---|---|---|

| F1 Enterprise Value | $8 billion | $26 billion+ | +225% |

| Average F1 team valuation | $300–400M | $1.88 billion (2024) | +376% in 4 years |

| Ferrari team valuation | ~$800M est. | $3.9 billion | ~+390% |

| Mercedes team valuation | ~$700M est. | $3.8 billion | ~+440% |

| Avg. sponsorship deal size | ~$2.87M (2019) | $5.08M (2024) | +77% |

| F1 % of global sports sponsorship | — | 6.6% | New record (2024) |

Table 4: Formula 1 Brand Valuation Data. Source: Liberty Media Corporation (NASDAQ: FWONA); BlackBook Motorsport (Dec 2024); Nielsen Sports Annual Report 2024; HuddleUp Newsletter (March 2026).

The average F1 team sponsorship deal doubled in size in five years, from $2.87 million in 2019 to $5.08 million in 2024 (BlackBook Motorsport, 2024). That is not because the cars became faster. It is because the audience became broader, younger, and more commercially desirable. Content built that audience. Brand value followed.

2.6 Calendar Expansion: Cities That Now Pay to Compete

The F1 race calendar expanded from 20 races in 2017 to 24 races in 2025, a steep 20% increase. But the calendar’s growth is less important than its geography. New races were not added in established European markets where the sport had always been popular. They were added in Miami, Las Vegas, Jeddah, Lusail, and from 2026, Madrid. These are markets where the new audience lives (Formula1.com Official Calendar, 2025).

In 2025, 19 of 24 events sold out completely. The Las Vegas Grand Prix alone generated 1.8 billion social media impressions and sold out its 300,000-person weekend capacity. The Miami Grand Prix produced $420 million in regional economic impact in its first year. A decade ago, no serious promoter would have placed a Grand Prix on the Las Vegas Strip. Calendar expansion is the commercial echo of a content strategy. New cities do not pay tens of millions to host a sporting event when the audience is in decline.

DATA LAYER 2

The Content Marketing Landscape

3.1 The $525 Billion Global Bet

Formula 1’s transformation is not an anomaly. It is the most visible example of a structural shift in how commercial relationships are built, which is a shift that is now reflected in a global content marketing market valued at over $525 billion in 2025, growing at 13.7% annually (Mordor Intelligence, 2025; Business Research Insights, 2025). At this trajectory, the market approaches $1 trillion by 2030 and could exceed $1.6 trillion by 2033.

$525B+Global content marketing market size, 2025

13.7%CAGR projected through 2033

3xMore leads vs traditional marketing

62%Less expensive than traditional marketing

Source: Mordor Intelligence (October 2025); Business Research Insights (2025); Content Marketing Institute Annual Report.

The return-on-investment data is striking in its consistency. Email content marketing returns $36 for every $1 spent. Organic search driven by content converts at 8.5 times the rate of outbound leads. Companies that maintain active blogs generate 57% more visitors, 67% more leads, earn 97% more inbound links, and have 434% more indexed pages than companies that do not (Backlinko, 2025; Content Marketing Institute, 2024). In 2024, 54% of businesses increased their content marketing spend, not because it was fashionable, but because it was working (Reboot Online, 2025).

3.2 The Buyer Who Has Already Decided

The most commercially important data point in this study is not about F1. It is about buyer behavior. Multiple independent studies, conducted across B2B purchasing decisions in multiple industries between 2020 and 2024, confirm a single, structural finding: B2B buyers complete approximately 70% of their purchasing process before they ever contact a sales representative (6sense, 2024; Forrester Research).

Read that again. By the time someone contacts your business, they have already made most of the decision, with or without your content. The question content strategy answers is whether they made that decision guided by your thinking or guided by a competitor’s.

| Finding | Statistic | Source |

|---|---|---|

| Buyers complete research before contacting sales | 57–70% | 6sense Buyer Experience Report 2024; Forrester |

| Buyers who have a preferred vendor at first contact | 81% | 6sense / Dreamdata B2B Benchmarks |

| Buyers who have defined requirements before reaching out | 85% | 6sense Buyer Experience Report 2024 |

| Buyers who start with the vendor they ultimately choose | 84% | Diginomica / 6sense Analysis |

| B2B buyers who initiate first contact themselves | 83% | 6sense Research |

| Average B2B buyer journey duration | 11.3 months | SurveyVista / Gartner |

| B2B buyers in a typical buying group (2025) | 11 people | Challenger Inc. / Gartner |

| Online content with ‘moderate to major’ effect on purchase | 9 in 10 B2B buyers | Worldwide Business Research |

Table 5: B2B Buyer Behavior Data. Source: 6sense 2024 Buyer Experience Report; Dreamdata B2B Benchmarks; Forrester Research; Gartner; Worldwide Business Research.

The 70% figure has circulated widely since a CEB/Google study in 2011–2013. A challenge by SiriusDecisions in 2015 briefly disputed it. Multiple independent studies conducted between 2020 and 2024, including 6sense’s analysis of live B2B purchasing data, consistently confirm a figure in the 57–70% range. The 2024 figure is 70%, up from 57% in 2020, suggesting self-directed research has intensified, not diminished (6sense, 2024). The buyer journey has also extended: the average B2B purchase now takes 11.3 months from initial research to signed contract.

“

If 84% of buyers start with the vendor they ultimately choose, your content is doing the selling before your sales team picks up the phone. This is not a trend. It is the standard operating model of commercial decision-making.

3.3 Why Educational Content Wins in Search

One of the most consistent findings in search performance data is that content which educates outperforms content which sells, particularly in organic search and, increasingly, in AI-generated answers. Research from Semrush, analyzing over 10 million keywords, found that 88.1% of queries triggering Google AI Overviews are informational in nature (Semrush, December 2025). In January 2025, that figure reached 91.3%, the highest recorded reading.

This is not a coincidence. It is the architecture of how people use search. They search to understand, not primarily to buy. The moment they know what they need, many of them have already decided who to buy from, which in most cases is guided by the content that answered their questions.

3.4 The Timeline Problem: Why Patience Is the Strategy

The single greatest misunderstanding about content marketing, and the reason most businesses abandon it before it works, is the timeline. Top-of-funnel content does not produce immediate commercial results. Neither did Drive to Survive. Season 1 launched in March 2019. The US Grand Prix attendance surge came in 2021. The ESPN rights explosion was negotiated in 2023. The demographic transformation was confirmed by the 2025 Fan Survey. The compounding played out over six years.

| Phase | Timeline | What Happens | F1 Parallel |

|---|---|---|---|

| Foundation | Month 1–3 | Content published; initial indexing | Drive to Survive S1 released (March 2019) |

| Traction | Month 4–8 | Organic traffic builds; AI tools begin citing | US viewership begins rising; social following grows |

| Commercial Signal | Month 6–12 | Inbound leads increase; brand awareness grows | US GP attendance surges in 2021; ESPN’s interest grows |

| ROI Materialises | Month 12–24 | Content KPIs connect to revenue metrics | ESPN rights 1,500% increase negotiated (2023) |

| Compounding | Year 2–5+ | Domain authority, AI citations accumulate | F1 enterprise value +114% by 2023 vs 2017 |

Table 6: Content Strategy Timeline vs F1 Parallel. Source: Skai.io Organic vs Paid Search Analysis; Conductor 2024 Organic Traffic Benchmarks; Liberty Media/Forbes F1 Valuation Timeline.

Organic search typically requires 4–12 months to demonstrate meaningful traction, varying by competition and existing domain authority (Conductor, 2024). Unlike paid campaigns, there is no end date for effective content. A well-optimized piece published today can generate leads for years. The business owner asking ‘Will this blog post get me customers next week?’ is asking the wrong question. The right question is: ‘Will the person who finds this in six months already trust me before they call?’

DATA LAYER 3

The AI Search Shift

4.1 The 87% Finding: What People Actually Ask AI Tools

The emergence of AI-mediated search — ChatGPT, Perplexity, Google AI Overviews, Claude, and other major LLMs — represents the most significant structural shift in information discovery since Google itself. It is also the shift that makes content strategy more urgent, not less. The reason can be reduced to a single finding.

WebSpero’s own cross-platform analysis, running structured query samples across ChatGPT, Perplexity, Google AI Overviews, and Claude, found that approximately 87% of real-world AI queries are informational in nature — people seeking to understand something, not to buy something (WebSpero Solutions, 2025). This finding is corroborated by multiple independent data sets: Semrush (88.1%), a joint OpenAI/Harvard study finding 53%+ of ChatGPT sessions are informational or guidance-seeking (OpenAI/Harvard, September 2025), and Google’s own AI Overview intent distribution data.

87%

of real-world AI queries are informational in nature — people seeking to understand something, not to buy something

of real-world AI queries are informational in nature — people seeking to understand something, not to buy something

88.1%AI Overviews queries informational (Semrush)

91.3%Peak reading — January 2025 (Semrush)

883MMonthly ChatGPT users January 2026

Source: WebSpero Solutions cross-platform query analysis (2024–2025); Semrush AI Overviews Study (December 2025); OpenAI/Harvard joint study (September 2025); Semrush clickstream analysis (April 2026).

The commercial implication is stark: if nearly 9 in 10 people opening ChatGPT or Perplexity are not there to buy something but to understand something, a business with nothing educational to offer is invisible to 9 in 10 of those people. Not hard to find — invisible.

4.2 How AI Decides What to Cite

The question of which content gets cited by AI tools is now one of the most commercially important questions in digital marketing. Research by SE Ranking in 2025, analyzing AI citation patterns at scale, identified the following factors as statistically significant:

| Citation Factor | Finding | Source |

|---|---|---|

| Content length | Articles over 2,900 words are 59% more likely to be cited than those under 800 words | SE Ranking (2025) |

| Section structure | Pages with 120 to 180 word sections earn 70% more citations than very short sections | SE Ranking (2025) |

| Content recency | Content updated within 3 months is 2x more likely to be cited than older pages | SE Ranking (2025) |

| Domain authority | Sites with 32K+ referring domains are 3.5x more likely to be cited | SE Ranking (2025) |

| Brand mentions (Reddit) | Sites with 35K+ Reddit mentions are significantly more likely to be cited | SE Ranking (2025) |

| Page speed | Pages with FCP <0.4s are 3x more likely to be cited than slow pages | SE Ranking (2025) |

| Data & statistics | Including facts/numbers increases citation likelihood by 40%+ | Princeton/University of Delhi (GEO Study) |

| Content tone | Promotional-first content is deprioritized; factual/objective is preferred | MarTech/Search Engine Land (2026) |

| AI-generated mass content | 87% drop in citation frequency after Google 2025 update | MarTech (2026) |

Table 7: AI Citation Factors. Source: SE Ranking AI Citation Study (2025); Princeton/University of Delhi GEO Paper; MarTech/Search Engine Land (2026).

The pattern is consistent: AI tools cite content that looks like journalism, not advertising. Factual. Structured. Sourced. Long enough to be genuinely useful. Written to answer a question, not to close a sale. This is not a coincidence — it mirrors precisely the kind of content that has always worked in organic search. AI has not changed the content quality standard. It has raised the stakes for meeting it.

4.3 The Sports Niche: An Underserved Opportunity

For sports content specifically, AI citation patterns reveal an interesting structural gap. According to Ahrefs’ November 2025 vertical breakdown data, only 14.8% of sports queries trigger AI Overviews compared with 43.6% for Science and 43.0% for Health (Ahrefs, November 2025). This means sports-adjacent informational content is still being predominantly answered by traditional blue-link results, representing competitive white space for brands operating in or around the sports and entertainment niche.

Wikipedia accounts for 43% of all ChatGPT citations in general queries, thus reflecting the platform’s role as a trusted, structured, well-sourced reference (Azoma.ai, August 2025). Reddit accounts for 12%, YouTube for 5%. In Google AI Overviews, Reddit leads at 20%, YouTube at 19%, and Quora at 14%. The common thread across all platforms: community-driven, question-answering content in trusted, structured contexts.

4.4 The Zero-Click World

The structural shift from traditional search to AI-mediated answers is not a future development. It is already the present reality. Google processed an estimated 9.1–13.6 billion searches per day in 2025, more than ever before (SparkToro/Datos, 2025). But 58.5% of those searches now end without a click to an external website. In Google AI Mode, the figure rises to 93% (SparkToro/Datos, 2025).

58.5%Google searches ending without a click (2025)

93%Zero-click rate in Google AI Mode

357%Growth in AI referral traffic Jun 2024–2025

73%B2B sites with AI-driven traffic loss 2024–2025

Source: SparkToro/Datos zero-click study (2025); exposureninja.com AI Search Statistics (Feb 2026); MarTech/Search Engine Land (March 2026).

Organic CTR for informational queries where an AI Overview is present dropped 61% year-on-year between June 2024 and September 2025 (MarTech, 2026). But when a brand is cited in an AI Overview, organic CTR is 35% higher than average (Search Engine Land, April 2026). The game is no longer exclusively about ranking in position one. It is about being the source the AI chooses to cite.

52% of US adults now use AI tools regularly (MarTech, 2026). Among Gen Z, 66% use ChatGPT versus 69% who use Google, near parity (Fractl, 2025). AI search visitors are projected to surpass traditional search visitors by 2028 (exposureninja.com, 2026). 73% of B2B websites saw significant organic traffic losses between 2024 and 2025, with an average year-on-year decline of 34% (MarTech, March 2026). The shift is not hypothetical. It is already inside the analytics dashboards of every business with a website.

05

Synthesis and Climax: The Convergence Point

Three separate analytical threads now converge in a single argument. The F1 story is the proof. The content marketing data is the context. The AI shift is the accelerant.

5.1 Three Shifts Arriving at the Same Moment

01

The Structural Shift

Buyers have taken control of the purchasing journey. With 70% of the B2B decision made before first contact, with 84% of buyers starting with the vendor they ultimately choose, the commercial conversation happens in content before it happens in conversation. This shift was underway before Drive to Survive was commissioned. It will not reverse.

02

The Technological Shift

AI has changed the architecture of information discovery. The 883 million monthly ChatGPT users, the 58.5% zero-click Google search rate, the 357% growth in AI referral traffic — these are not emerging trends. They are the current operating conditions. The businesses being cited in AI answers today are building compounding commercial advantages that their competitors will struggle to close.

03

The Demographic Shift

The largest consumer generation in history — Gen Z — discovers, evaluates, and chooses products through content-first pathways. They do not respond to interruption advertising. They do not pick up cold calls. They search, they watch, they read, they scroll, and they trust the brand that educated them before asking them to buy. F1’s 34-percentage-point female fanbase increase is the most dramatic demonstration of this principle in modern business history.

“

The convergence of these three shifts — self-directed buyers, AI-mediated discovery, and the Gen Z economy — means that educational content is no longer a marketing tactic. It is the primary channel through which trust is built before commerce begins.

5.2 The Small Business Imperative

Formula 1 had $1.8 billion in revenue when it began its content transformation. The lesson of Drive to Survive is not about Netflix budgets. It is about intent. The intent was specific: make content for the person who has never heard of you yet. Not the person who already loves you. Not the person who is almost ready to buy. The person who does not yet know they are in your market.

For a small business, the practical translation is straightforward. The podcast episode that explains what your business actually does. The blog post that answers the question your best customers always ask first. The plain-English guide that removes the jargon your industry has always hidden behind. These are the Drive to Survive episodes of your brand. You do not need a Netflix production budget. You need the intent: to be genuinely useful to someone who has never heard of you.

The data on AI citations makes this even more specific. Content that is over 2,900 words is 59% more likely to be cited (SE Ranking, 2025). Content updated within three months is twice as likely to be cited. Content that includes facts and data increases citation likelihood by 40%. The AI citation algorithm is, functionally, a usefulness filter. Useful, detailed, factual, educational content wins. Everything else loses.

5.3 The Formula

The following synthesis is not a hypothesis. It is derived from the convergence of three independently verified data layers in this study.

Action

F1 Parallel

Commercial Outcome

1

ActionIdentify the person who doesn’t know they need you yet. Build content for them, not for your existing customers.

F1 ParallelDrive to Survive was made for people who had never watched a Grand Prix.

Commercial OutcomeNew audience segment created; global fanbase grew from ~500M to 827M.

2

ActionMake educational content the default, not the exception. Answer questions before they become sales conversations.

F1 ParallelBehind-the-scenes driver profiles; team explainers; technical breakdowns in accessible language.

Commercial Outcome81% of buyers arrive with a preferred vendor — be that vendor. Content positions you as the trusted source before any sales conversation occurs.

3

ActionDistribute consistently and across formats. Stories work because they compound.

F1 ParallelNetflix documentary + social media + YouTube + F1TV together, not separately.

Commercial OutcomeSocial following: 18.7M → 107.6M (+475%). Multi-format, sustained distribution compounds reach and brand authority over time.

4

ActionStructure content so AI can cite it. Long, factual, sourced, and recently updated.

F1 ParallelF1.com editorial strategy: data-rich, authoritative, regularly updated.

Commercial OutcomeCitation in AI answers = 35% higher CTR vs average organic. Being the source AI cites builds compounding discovery advantages that competitors cannot easily close.

5

ActionMeasure over the right timeframe. Content that educates builds trust over months, not days.

F1 ParallelESPN’s rights 1,500% increase came 5 years after the content strategy began.

Commercial OutcomeOrganic content: the only channel that produces reliable long-term, compounding returns. Domain authority, AI citations, and inbound leads accumulate — no end date for effective content.

Table 8: The Formula 1 Effect — Applied Framework for Content Strategy.

Section 06 · The Climax

The Question That

The Question That

Changes Everything

In 2016, Formula 1 was asking the wrong question. Its executives were asking: How do we improve the racing? How do we make the cars more spectacular? How do we make the sport more technically impressive? These were reasonable questions. None of them produced the growth. The growth came when Liberty Media arrived and asked a different question entirely:

“Who are we not talking to yet, and what story do they need to hear?”

That question produced a chain reaction

Drive to SurviveThe story

→

700M viewersThe reach

→

827M fansThe audience

→

$26B enterprise valueThe outcome

$26 billion in enterprise value was built not from faster cars or better circuits or higher prize money. It was built from stories told to people who didn’t yet know they were an audience.

The AI search shift makes this question more urgent than it has ever been. When 87% of AI queries are informational, when 58.5% of Google searches end without a click, when Gen Z turns to ChatGPT at nearly the same rate as Google, the brands that win are not the ones that shout loudest. They are the ones who got there first with the most useful answer. They wrote the educational content before everyone else started trying. They built the domain authority before it became expensive. They became the source that the AI cites before the AI became the dominant discovery channel.

The buyer behavior data seals the argument. 84% of B2B buyers start with the vendor they ultimately choose. 81% have a preferred vendor before first contact. 85% have already defined their requirements. The sales conversation, the one businesses have been optimizing for decades, happens after the decision. The content conversation is where the decision is made.

Formula 1 was not a technology story. It was not a regulatory story. It was not even, ultimately, a sports story. It was a content strategy story — the most commercially documented, independently verified, globally visible proof that storytelling is the most powerful commercial lever available to any business, regardless of size.

The sport that was dying because nobody outside its existing fanbase knew why they should care tripled its enterprise value in eight years. It did not improve its product. It improved its story. It did not find new customers. It found new audiences and trusted that, given a reason to care, those audiences eventually become customers.

References

Layer 1 — Formula 1 Sources

- [1] Liberty Media Corporation (2017, 2024, 2025). Annual Reports and Press Releases (NASDAQ: FWONA, FWONK). libertymedia.com/investors

- [2] BlackBook Motorsport (2026, March). F1 revenue grows 14% YoY to US$3.87bn in 2025.

- [3] BlackBook Motorsport (2024, December). F1 named most popular annual sports series with over 750 million fans.

- [4] S&P Global Market Intelligence (2025, August). Formula One revenue up 5.9% in 2024.

- [5] HuddleUp Substack (2026, March). How Formula 1 Makes Money: A Complete Business Breakdown Before The 2026 Season.

- [6] Nielsen Fan Insights (2022, May). Driven to watch: How a sports docuseries drove U.S. fans to Formula 1.

- [7] Nielsen Sports Annual Report (2024). Global sports sponsorship and fan engagement data.

- [8] Plum Research / ShowLabs (2022, October). Drive to Survive: How Netflix Ignited the Love for Formula 1 in the United States. Medium.

- [9] Parrot Analytics (2019–2025). Formula 1: Drive to Survive — audience demand data.

- [10] Domo (2026, May). Drive to Survive by the Numbers: A Domo Analysis of Season 8 Data.

- [11] F1 / Motorsport Network (2025, July). 2025 Global F1 Fan Survey — 100,000+ responses, 186 countries.

- [12] Newsweek (2025, August). Formula 1 Is Exploding in Popularity Among Women.

- [13] Comscore (2025, April). The Changing Face of Formula 1.

- [14] F1 CEO Stefano Domenicali — public statements on female fanbase (various, 2023–2025).

- [15] Formula1.com — Official race calendar and press releases, 2017–2025.

- [16] The-Race.com (2026, February). F1 race contracts: How long will each track stay on the calendar?

- [17] University of Miami Study (2022). 2022 Miami GP economic impact analysis.

- [18] Forbes (2017, 2025). Formula 1 enterprise valuation.

Layer 2 — Content Marketing Sources

- [1] Mordor Intelligence (2025, October). Content Marketing Market Size & Share Outlook to 2030.

- [2] Business Research Insights (2025). Content Marketing Market Size, Share & Growth 2025 to 2033.

- [3] Content Marketing Institute. Annual B2B Content Marketing Report.

- [4] Reboot Online (2025, June). Content Marketing Statistics.

- [5] Backlinko (2025). Organic search benchmarks and blog traffic data.

- [6] 6sense (2024). Buyer Experience Report — primary research into B2B purchasing behavior.

- [7] Dreamdata. B2B Go-to-Market Benchmarks.

- [8] Forrester Research. B2B buyer journey self-direction data.

- [9] Diginomica (2023, December). When you get to the 70% mark in a B2B journey, nothing is going to change the buyer’s mind.

- [10] SurveyVista (2025, August). B2B Buyer Journey Feedback That Drives Growth.

- [11] Gartner. B2B buyer group size and journey duration benchmarks.

- [12] Challenger Inc. B2B buying group composition data (2025).

- [13] Worldwide Business Research. Online content effect on purchase decisions.

- [14] Conductor (2024). Organic Search Traffic Benchmarks Report.

- [15] Skai.io (2025, January). Organic Search Marketing vs Paid Search Advertising.

Layer 3 — AI Search Sources

- [1] Semrush (2025, December). AI Overviews Study: What 2025 SEO Data Tells Us About Google’s Search Shift (10M+ keyword analysis).

- [2] Semrush (2026, April). ChatGPT traffic analysis: Insights from 17 months of clickstream data.

- [3] Semrush (2025, November). 26 AI SEO Statistics for 2026.

- [4] SE Ranking (2026, January). 70+ AI Search Stats for 2026 — citation factor research.

- [5] OpenAI & Harvard (2025, September). Joint study on ChatGPT use cases and intent classification.

- [6] Ahrefs (2025, November). AI Overview vertical breakdown data.

- [7] Azoma.ai (2025, August). The Sources ChatGPT and Google AI Overviews Cite the Most, Per Query Type.

- [8] SparkToro / Datos (2025). Zero-click search study.

- [9] MarTech / Search Engine Land (2026, March). Organic search is fundamentally disrupted. Here’s what to do about it.

- [10] Search Engine Land (2026, April). AI Overviews optimization guide — citing Princeton/University of Delhi GEO paper.

- [11] Fractl (2025). Gen Z search behavior: ChatGPT vs Google.

- [12] exposureninja.com (2026, February). AI Search Statistics for 2026: CMO Cheatsheet.

- [13] WebSpero Solutions (2024–2025). Cross-platform AI query intent analysis: ChatGPT, Perplexity, Google AI Overviews, Claude.

This research study was compiled in May 2026. All third-party data cited under principles of fair use for research and commentary purposes. Every major claim is cross-referenced by at least two independent sources. The analysis and narrative synthesis are original to this study. Data current as of Q1 2026.